The Basel III Catalyst: How Physical Capital is Becoming the New Foundation for Leverage

In 2024, central banks purchased over 1,000 tonnes of gold for the third consecutive year. While this historic accumulation is often framed as a defensive maneuver, sophisticated institutions understand it differently: it is a strategic optimization of balance sheet capital. Sovereign entities are acquiring physical assets not out of fear, but because the regulatory architecture of global finance is actively rewarding capital efficiency.

The Basel III Catalyst

How Physical Capital is Becoming the New Foundation for Leverage

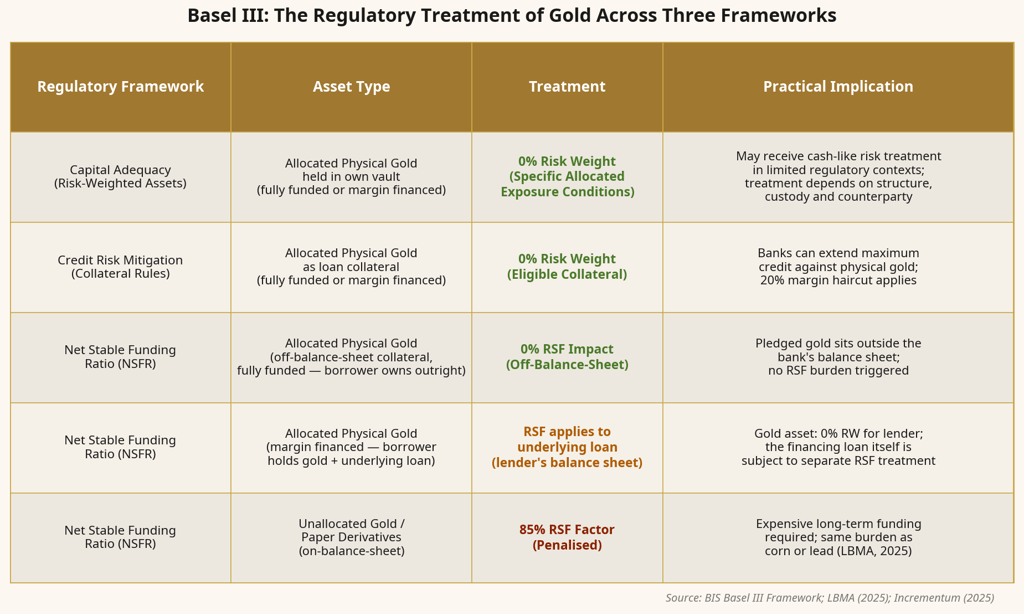

Figure 1: Basel III Regulatory Treatment of Gold Across Three Frameworks

The Evolution of Credit and Performance-Driven Leverage

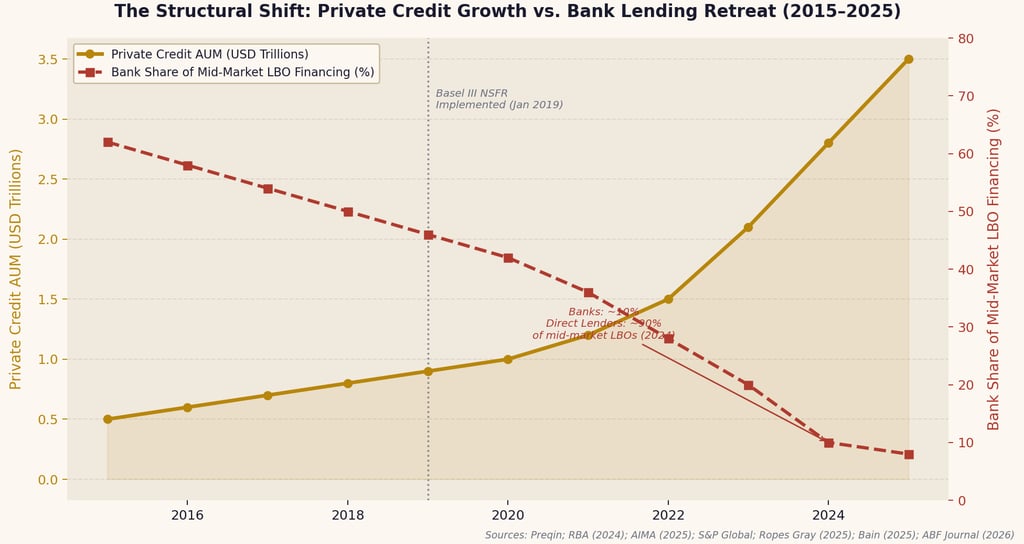

This regulatory push for balance sheet discipline extends directly into credit markets. To optimize their capital charges, traditional banks are becoming more selective, moving away from unsecured middle-market lending and demanding higher Loan-to-Value (LTV) ratios backed by real collateral.

This evolution has created a robust opportunity for private credit and structured finance. Credit is not disappearing; it is being reallocated toward performance and quality. The new standard for leverage is proven cash flow and capital-efficient collateral.

Structures backed by allocated physical gold, where favourable Basel III risk weighting conditions are met, benefit from a structurally lower cost of capital because they align with the regulatory premium placed on unencumbered, zero-counterparty-risk collateral.

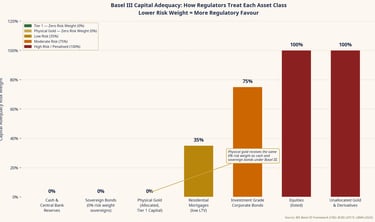

Figure 2: The Regulatory Penalty on Assets (NSFR / RSF Factors)

Figure 3: The Structural Shift in Middle-Market Lending

The Bond Evolution: Complementing the Traditional Safe Haven

The conventional institutional portfolio is built on the 60/40 model: equities for growth, bonds for safety and income. Sovereign bonds remain a cornerstone of global finance and continue to enjoy a highly favored 0% risk weight under Basel III.

However, the current macroeconomic environment, characterized by persistent inflation and elevated sovereign debt levels, is prompting institutions to diversify their reserve strategies. While bonds provide essential yield, inflation can erode their real return, and rising interest rates can impact their capital value.

In this environment, physical gold serves as a powerful complement to sovereign bonds. It offers scarcity and zero counterparty risk, providing a different dimension of capital efficiency. The historical challenge for gold has simply been its lack of yield, a challenge that modern structured finance is now solving.

Market Volatility and the Opportunity Cost of Static Assets

The recent volatility in the gold market perfectly illustrates the tension between physical scarcity and the demand for yield. In early 2026, after surging to historic highs, gold experienced a sharp correction. This sudden drop was not a structural failure of the asset, but a rational market response to shifting interest rate expectations.

As central banks maintained a "higher-for-longer" stance, the opportunity cost of holding a non-yielding asset increased. This prompted a rotation out of static gold positions and into yield-bearing instruments. The vulnerability highlighted here is not gold's physical nature, but the traditional approach of holding it as a static, non-yielding reserve. To truly harness its capital efficiency, gold must be put to work.

The Leverage Trap: Why Equity Exposure is Not the Answer

In an attempt to generate yield or leverage from gold, many investors turn to gold mining equities. However, recent market action demonstrated the structural risks of this approach. Miners are essentially leveraged bets on the gold price, carrying significant operational and equity market risks.

During periods of volatility, miners can face a dual squeeze: falling revenues due to gold price fluctuations, and rising operating costs driven by energy prices. Furthermore, in a volatile environment, equities are often sold to meet margin calls elsewhere. This proves that equity exposure is a highly volatile proxy for physical wealth, lacking the pristine capital efficiency that Basel III rewards in allocated gold.

Digital Assets and the Same Paper Cycle

The structural logic of Basel III also provides a constructive lens for evaluating digital assets. Bitcoin and the broader crypto market began as a decentralized alternative, but the financial industry quickly built a layer of paper abstraction on top of them: ETFs, futures contracts, and centralized exchanges.

Regulators are applying the same logic to digital assets as they do to gold: direct, unencumbered ownership is preferred, while paper abstractions and synthetic exposures are penalized. The Basel Committee has proposed conservative risk weights for unbacked crypto assets, reinforcing the principle that capital efficiency requires minimizing counterparty risk.

Like static gold, digital assets also face the volatility-yield trap. Because they generate no intrinsic yield, they are dependent on price appreciation and face rotation pressure when interest rates rise. The lesson across all asset classes is consistent: the regulatory premium belongs to direct ownership, and that ownership must be engineered to generate yield.

The Price Drop Fallacy: Why Spot Volatility Misses the Point

The frenzy surrounding short-term spot price drops often conflates two fundamentally different concepts: the daily trading price of paper gold and the structural, regulatory premium placed on physical ownership. Recent price drops were liquidity events driven by leveraged investors adjusting paper and equity positions, not a change in the asset's fundamental utility.

"The true value of physical capital lies not in its daily spot price, but in its capacity to anchor leverage and generate yield."

In 2024, central banks purchased over 1,000 tonnes of gold for the third consecutive year. While this historic accumulation is often framed as a defensive maneuver, sophisticated institutions understand it differently: it is a strategic optimization of balance sheet capital. Sovereign entities are acquiring physical assets not out of fear, but because the regulatory architecture of global finance is actively rewarding capital efficiency.

For decades, institutional portfolios relied heavily on synthetic derivatives, rehypothecation, and unsecured credit to generate yield and manage risk. However, the prolonged implementation of the Basel III regulatory framework, often referred to as the "Basel III Endgame," is evolving the rules of liquidity and capital adequacy.

Basel III is not a mandate for a return to a gold standard, nor does it signal systemic fragility. Rather, it is a framework designed to enforce balance sheet discipline and minimize counterparty risk. By imposing stringent capital requirements on opaque or leveraged assets, regulators are actively making synthetic exposure more expensive. The result is a constructive, structural repricing: capital is migrating toward efficient, low-risk assets that provide a real foundation for leverage and growth.

The Regulatory Premium on Capital Efficiency

The most profound impact of Basel III on real-asset markets lies in its treatment of capital adequacy and liquidity. The framework draws a sharp distinction based on counterparty risk, rewarding assets that are unencumbered and directly held.

Under the Net Stable Funding Ratio (NSFR), unallocated gold, paper derivatives, and synthetic exposures are treated as liabilities of a financial institution. Because they carry counterparty risk, they require an 85% Required Stable Funding (RSF) factor. This means banks must hold substantial, expensive long-term funding to back these paper positions.

Conversely, allocated physical gold held unencumbered in a vault carries zero counterparty risk. Under the Basel III capital adequacy framework, allocated gold exposures may receive a 0% credit risk weight under specific structural conditions, making it one of the most capital-efficient collateral assets available, comparable in risk treatment to cash in qualifying contexts.

This regulatory treatment fundamentally changes the role of physical gold. It is no longer just a passive store of value; it is a highly capital-efficient asset. For institutions and structured finance vehicles, this 0% risk weight means that allocated gold can serve as an exceptional, low-cost collateral base for securing leverage and funding productive economic activity.

Published by: Research and Insights team at 168 Capital

This research insight is provided by 168 Capital, a private firm dedicated to real-asset income and durable wealth through a closed-loop system spanning gold, land, real estate, and essential commodities. This document is for educational and informational purposes only and does not constitute investment advice.

EXECUTIVE TAKEAWAYS

Allocated physical gold may receive a 0% credit risk weight under the Basel III capital adequacy framework under specific conditions, including allocated custody structure, counterparty treatment, and jurisdiction. This places it among the most capital-efficient collateral assets available to lenders.

This regulatory treatment transforms physical gold from a static reserve into a highly capital-efficient asset, making it an ideal foundation for institutional leverage.

As credit markets tighten and demand pristine collateral, structures backed by allocated physical gold, where favourable risk weighting applies, benefit from a structurally lower cost of capital relative to synthetic or unsecured exposures.

The true opportunity lies in engineering yield: converting the capital efficiency of physical gold into a predictable cash flow through active, structured deployment.

Crucially, the Basel III architecture has not changed its position. Regulators did not revise the 0% risk weight on physical gold when the price fluctuated. Investors holding allocated physical gold through a yield-generating structure experience price volatility as background noise because their return is driven by operational throughput, not the spot price.

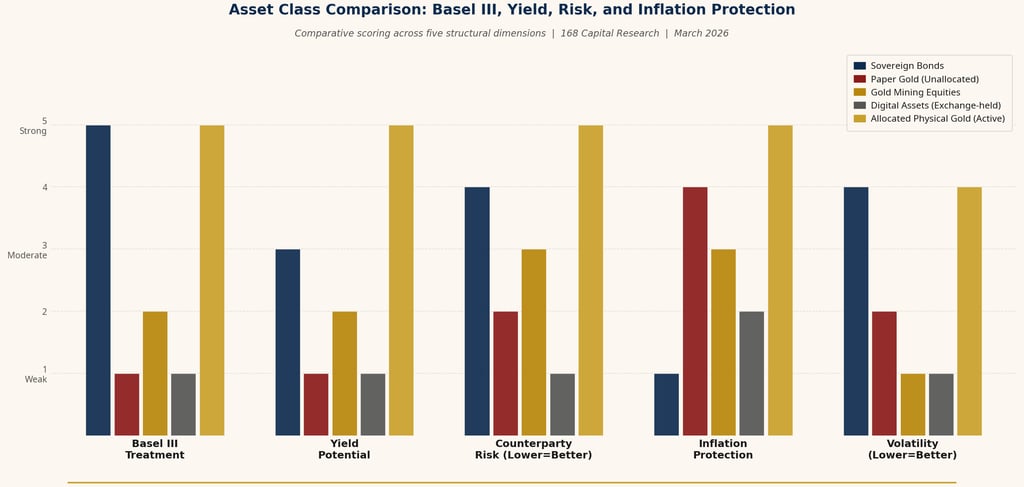

The Structural Framework: Comparing Asset Exposure

When evaluated through the lens of Basel III treatment, yield potential, and capital efficiency, the strategic advantage of active physical ownership becomes clear. The following framework compares the primary methods of accessing safe-haven and alternative assets:

Figure 4: Asset Class Comparison Across Five Structural Dimensions

Conclusion: The Structural Premium on Physical Capital

The transition mandated by Basel III represents a formal regulatory recognition of a broader macroeconomic reality: sustainable leverage must be built on a foundation of capital-efficient, low-risk assets. As counterparty risk becomes more expensive and balance sheet discipline tightens, capital is migrating toward assets that are financeable and real.

However, the critical lesson of the current macro environment is that capital efficiency alone is not enough. To thrive in a high-rate regime, physical assets cannot be relegated to static reserves. They must be engineered to generate stable, provable cash flow.

This is the structural logic behind initiatives like the Gold-Backed Income and Ownership Program (G-BIP). By anchoring securitization in allocated physical gold, structured to qualify for favourable Basel III capital treatment, and controlling the physical flow end-to-end...

In an environment where regulators are rewarding balance sheet discipline and markets are demanding bankable performance, the most durable allocations will be those built on assets that are real, scarce, and structurally favoured by the framework that governs global capital. Physical gold, deployed with precision and purpose, is what anchors the next generation of wealth.

© .168 Capital 2025

This site is published for informational purposes only. It describes the operational architecture and supply chain framework of 168 Capital and its subsidiaries. Nothing on this page constitutes an offer, solicitation, or invitation to enter into any agreement of any kind. 168 Capital does not solicit counterparties through public channels. All bilateral engagements are established through direct, private contact and are subject to due diligence and the execution of definitive agreements.

SOCIAL MEDIA

Building tomorrows real-asset economy